This example has been auto-generated from the examples/ folder at GitHub repository.

Autoregressive Models

# Activate local environment, see `Project.toml`

import Pkg; Pkg.activate(".."); Pkg.instantiate();In this example we are going to perform an automated Variational Bayesian Inference for a latent autoregressive model that can be represented as following:

\[\begin{aligned} p(\gamma) &= \mathrm{Gamma}(\gamma|a, b),\\ p(\mathbf{\theta}) &= \mathcal{N}(\mathbf{\theta}|\mathbf{\mu}, \Sigma),\\ p(x_t|\mathbf{x}_{t-1:t-k}) &= \mathcal{N}(x_t|\mathbf{\theta}^{T}\mathbf{x}_{t-1:t-k}, \gamma^{-1}),\\ p(y_t|x_t) &= \mathcal{N}(y_t|x_t, \tau^{-1}), \end{aligned}\]

where $x_t$ is a current state of our system, $\mathbf{x}_{t-1:t-k}$ is a sequence of $k$ previous states, $k$ is an order of autoregression process, $\mathbf{\theta}$ is a vector of transition coefficients, $\gamma$ is a precision of state transition process, $y_k$ is a noisy observation of $x_k$ with precision $\tau$.

For a more rigorous introduction to Bayesian inference in Autoregressive models we refer to Albert Podusenko, Message Passing-Based Inference for Time-Varying Autoregressive Models.

We start with importing all needed packages:

using RxInfer, Distributions, LinearAlgebra, Random, Plots, BenchmarkTools, ParametersLet's generate some synthetic dataset, we use a predefined sets of coeffcients for $k$ = 1, 3 and 5 respectively:

# The following coefficients correspond to stable poles

coefs_ar_1 = [-0.27002517200218096]

coefs_ar_2 = [0.4511170798064709, -0.05740081602446657]

coefs_ar_5 = [0.10699399235785655, -0.5237303489793305, 0.3068897071844715, -0.17232255282458891, 0.13323964347539288];function generate_ar_data(rng, n, θ, γ, τ)

order = length(θ)

states = Vector{Vector{Float64}}(undef, n + 3order)

observations = Vector{Float64}(undef, n + 3order)

γ_std = sqrt(inv(γ))

τ_std = sqrt(inv(τ))

states[1] = randn(rng, order)

for i in 2:(n + 3order)

states[i] = vcat(rand(rng, Normal(dot(θ, states[i - 1]), γ_std)), states[i-1][1:end-1])

observations[i] = rand(rng, Normal(states[i][1], τ_std))

end

return states[1+3order:end], observations[1+3order:end]

endgenerate_ar_data (generic function with 1 method)# Seed for reproducibility

seed = 123

rng = MersenneTwister(seed)

# Number of observations in synthetic dataset

n = 500

# AR process parameters

real_γ = 1.0

real_τ = 0.5

real_θ = coefs_ar_5

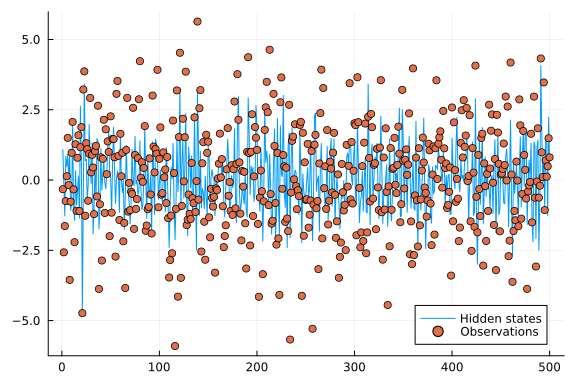

states, observations = generate_ar_data(rng, n, real_θ, real_γ, real_τ);Let's plot our synthetic dataset:

plot(first.(states), label = "Hidden states")

scatter!(observations, label = "Observations")

Next step is to specify probabilistic model, inference constraints and run inference procedure with RxInfer. We will specify two different models for Multivariate AR with order $k$ > 1 and for Univariate AR (reduces to simple State-Space-Model) with order $k$ = 1.

@model function lar_model(T, y, order, c, τ)

# Prior for first state

if T === Multivariate

γ ~ Gamma(α = 1.0, β = 1.0)

θ ~ MvNormal(μ = zeros(order), Λ = diageye(order))

x0 ~ MvNormal(μ = zeros(order), Λ = diageye(order))

else

γ ~ Gamma(α = 1.0, β = 1.0)

θ ~ Normal(μ = 0.0, γ = 1.0)

x0 ~ Normal(μ = 0.0, γ = 1.0)

end

x_prev = x0

for i in eachindex(y)

x[i] ~ AR(x_prev, θ, γ)

if T === Multivariate

y[i] ~ Normal(μ = dot(c, x[i]), γ = τ)

else

y[i] ~ Normal(μ = c * x[i], γ = τ)

end

x_prev = x[i]

end

end@constraints function ar_constraints()

q(x0, x, θ, γ) = q(x0, x)q(θ)q(γ)

endar_constraints (generic function with 1 method)@meta function ar_meta(artype, order, stype)

AR() -> ARMeta(artype, order, stype)

endar_meta (generic function with 1 method)@initialization function ar_init(morder)

q(γ) = GammaShapeRate(1.0, 1.0)

q(θ) = MvNormalMeanPrecision(zeros(morder), diageye(morder))

endar_init (generic function with 1 method)morder = 5

martype = Multivariate

mc = ReactiveMP.ar_unit(martype, morder)

mconstraints = ar_constraints()

mmeta = ar_meta(martype, morder, ARsafe())

moptions = (limit_stack_depth = 100, )

mmodel = lar_model(T=martype, order=morder, c=mc, τ=real_τ)

mdata = (y = observations, )

minitialization = ar_init(morder)

mreturnvars = (x = KeepLast(), γ = KeepEach(), θ = KeepEach())

# First execution is slow due to Julia's initial compilation

# Subsequent runs will be faster (benchmarks are below)

mresult = infer(

model = mmodel,

data = mdata,

constraints = mconstraints,

meta = mmeta,

options = moptions,

initialization = minitialization,

returnvars = mreturnvars,

free_energy = true,

iterations = 50,

showprogress = false

);@unpack x, γ, θ = mresult.posteriorsDict{Symbol, Vector} with 3 entries:

:γ => GammaShapeRate{Float64}[GammaShapeRate{Float64}(a=251.0, b=47.5918)

, Ga…

:θ => MvNormalWeightedMeanPrecision{Float64, Vector{Float64}, Matrix{Floa

t64}…

:x => MvNormalWeightedMeanPrecision{Float64, Vector{Float64}, Matrix{Floa

t64}…We will use different initial marginals depending on type of our AR process

p1 = plot(first.(states), label="Hidden state")

p1 = scatter!(p1, observations, label="Observations")

p1 = plot!(p1, first.(mean.(x)), ribbon = first.(std.(x)), label="Inferred states", legend = :bottomright)

p2 = plot(mean.(γ), ribbon = std.(γ), label = "Inferred transition precision", legend = :topright)

p2 = plot!([ real_γ ], seriestype = :hline, label = "Real transition precision")

p3 = plot(mresult.free_energy, label = "Bethe Free Energy")

plot(p1, p2, p3, layout = @layout([ a; b c ]))

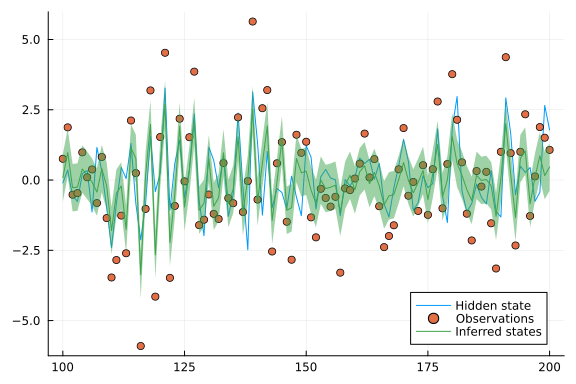

Let's also plot a subrange of our results:

subrange = div(n,5):(div(n, 5) + div(n, 5))

plot(subrange, first.(states)[subrange], label="Hidden state")

scatter!(subrange, observations[subrange], label="Observations")

plot!(subrange, first.(mean.(x))[subrange], ribbon = sqrt.(first.(var.(x)))[subrange], label="Inferred states", legend = :bottomright)

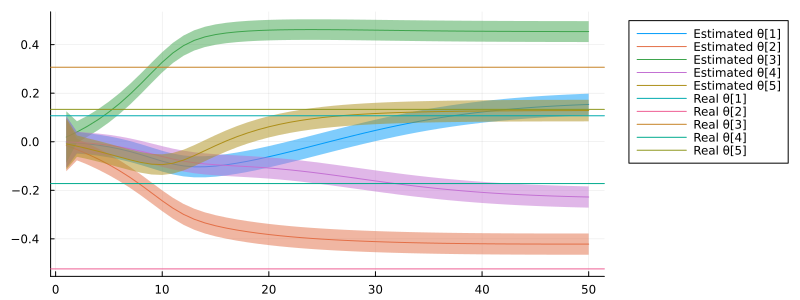

It is also interesting to see where our AR coefficients converge to:

let

pθ = plot()

θms = mean.(θ)

θvs = var.(θ)

l = length(θms)

edim(e) = (a) -> map(r -> r[e], a)

for i in 1:length(first(θms))

pθ = plot!(pθ, θms |> edim(i), ribbon = θvs |> edim(i) .|> sqrt, label = "Estimated θ[$i]")

end

for i in 1:length(real_θ)

pθ = plot!(pθ, [ real_θ[i] ], seriestype = :hline, label = "Real θ[$i]")

end

plot(pθ, legend = :outertopright, size = (800, 300))

end

println("$(length(real_θ))-order AR inference Bethe Free Energy: ", last(mresult.free_energy))5-order AR inference Bethe Free Energy: 1024.077566129808We can also run a 1-order AR inference on 5-order AR data:

uorder = 1

uartype = Univariate

uc = ReactiveMP.ar_unit(uartype, uorder)

uconstraints = ar_constraints()

umeta = ar_meta(uartype, uorder, ARsafe())

uoptions = (limit_stack_depth = 100, )

umodel = lar_model(T=uartype, order=uorder, c=uc, τ=real_τ)

udata = (y = observations, )

initialization = @initialization begin

q(γ) = GammaShapeRate(1.0, 1.0)

q(θ) = NormalMeanPrecision(0.0, 1.0)

end

ureturnvars = (x = KeepLast(), γ = KeepEach(), θ = KeepEach())

uresult = infer(

model = umodel,

data = udata,

meta = umeta,

constraints = uconstraints,

initialization = initialization,

returnvars = ureturnvars,

free_energy = true,

iterations = 50,

showprogress = false

);println("1-order AR inference Bethe Free Energy: ", last(uresult.free_energy))1-order AR inference Bethe Free Energy: 1025.8792949319945if uresult.free_energy[end] > mresult.free_energy[end]

println("We can see that, according to final Bethe Free Energy value, in this example 5-order AR process can describe data better than 1-order AR.")

else

error("AR-1 performs better than AR-5...")

endWe can see that, according to final Bethe Free Energy value, in this exampl

e 5-order AR process can describe data better than 1-order AR.Autoregressive Moving Average Model

Bayesian ARMA model can be effectively implemeted in RxInfer.jl. For theoretical details on Varitional Inference for ARMA model, we refer the reader to the following paper. The Bayesian ARMA model can be written as follows:

\[\begin{aligned} e_t \sim \mathcal{N}(0, \gamma^{-1}) \quad \theta &\sim \mathcal{MN}(\mathbf{0}, \mathbf{I}) \quad \eta \sim \mathcal{MN}(\mathbf{0}, \mathbf{I}) \\ \mathbf{h}_0 &\sim \mathcal{MN}\left(\begin{bmatrix} e_{-1} \\ e_{-2} \end{bmatrix}, \mathbf{I}\right) \\ \mathbf{h}_t &= \mathbf{S}\mathbf{h}_{t-1} + \mathbf{c} e_{t-1} \\ \mathbf{x}_t &= \boldsymbol{\theta}^\top\mathbf{x}_{t-1} + \boldsymbol{\eta}^\top\mathbf{h}_{t} + e_t \end{aligned}\]

where shift matrix $\mathbf{S}$ is

\[\begin{aligned} \mathbf{S} = \begin{pmatrix} 0 & 0 \\ 1 & 0 \end{pmatrix} \end{aligned}\]

and unit vector $\mathbf{c}$:

\[\begin{aligned} \mathbf{c}=[1, 0] \end{aligned}\]

when MA order is $2$

In this way, $\mathbf{h}_t$ containing errors $e_t$ can be viewed as hidden state.

In short, the Bayesian ARMA model has two intractabilities: (1) induced by the multiplication of two Gaussian RVs, i.e., $\boldsymbol{\eta}^\top\mathbf{h}_{t}$, (2) induced by errors $e_t$ that prevents analytical update of precision parameter $\gamma$ (this can be easily seen when constructing the Factor Graph, i.e. there is a loop). Both problems can be easily resolved in RxInfer.jl, by creating a hybrid inference algorithm based on Loopy Variational Message Passing.

# Load packages

using RxInfer, LinearAlgebra, CSV, DataFrames, Plots# Define shift function

function shift(dim)

S = Matrix{Float64}(I, dim, dim)

for i in dim:-1:2

S[i,:] = S[i-1, :]

end

S[1, :] = zeros(dim)

return S

endshift (generic function with 1 method)@model function ARMA(x, x_prev, h_prior, γ_prior, τ_prior, η_prior, θ_prior, c, b, S)

# priors

γ ~ γ_prior

η ~ η_prior

θ ~ θ_prior

τ ~ τ_prior

# initial

h_0 ~ h_prior

z[1] ~ AR(h_0, η, τ)

e[1] ~ Normal(mean = 0.0, precision = γ)

x[1] ~ dot(b, z[1]) + dot(θ, x_prev[1]) + e[1]

h_prev = h_0

for t in 1:length(x)-1

e[t+1] ~ Normal(mean = 0.0, precision = γ)

h[t] ~ S*h_prev + b*e[t]

z[t+1] ~ AR(h[t], η, τ)

x[t+1] ~ dot(z[t+1], b) + dot(θ, x_prev[t]) + e[t+1]

h_prev = h[t]

end

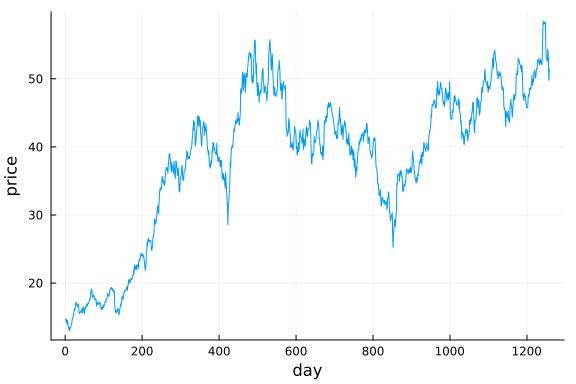

endTo validate our model and inference, we will use American Airlines stock data downloaded from Kaggle

x_df = CSV.read("../data/arma/aal_stock.csv", DataFrame)1259×7 DataFrame

Row │ date open high low close volume Name

│ Date Float64 Float64 Float64 Float64 Int64 String3

──────┼───────────────────────────────────────────────────────────────────

1 │ 2013-02-08 15.07 15.12 14.63 14.75 8407500 AAL

2 │ 2013-02-11 14.89 15.01 14.26 14.46 8882000 AAL

3 │ 2013-02-12 14.45 14.51 14.1 14.27 8126000 AAL

4 │ 2013-02-13 14.3 14.94 14.25 14.66 10259500 AAL

5 │ 2013-02-14 14.94 14.96 13.16 13.99 31879900 AAL

6 │ 2013-02-15 13.93 14.61 13.93 14.5 15628000 AAL

7 │ 2013-02-19 14.33 14.56 14.08 14.26 11354400 AAL

8 │ 2013-02-20 14.17 14.26 13.15 13.33 14725200 AAL

⋮ │ ⋮ ⋮ ⋮ ⋮ ⋮ ⋮ ⋮

1253 │ 2018-01-30 52.45 53.05 52.36 52.59 4741808 AAL

1254 │ 2018-01-31 53.08 54.71 53.0 54.32 5962937 AAL

1255 │ 2018-02-01 54.0 54.64 53.59 53.88 3623078 AAL

1256 │ 2018-02-02 53.49 53.99 52.03 52.1 5109361 AAL

1257 │ 2018-02-05 51.99 52.39 49.75 49.76 6878284 AAL

1258 │ 2018-02-06 49.32 51.5 48.79 51.18 6782480 AAL

1259 │ 2018-02-07 50.91 51.98 50.89 51.4 4845831 AAL

1244 rows omitted# we will use "close" column

x_data = filter(!ismissing, x_df[:, 5]);# Plot data

plot(x_data, xlabel="day", ylabel="price", label=false)

p_order = 10 # AR

q_order = 4 # MA4# Training set

train_size = 1000

x_prev_train = [Float64.(x_data[i+p_order-1:-1:i]) for i in 1:length(x_data)-p_order][1:train_size]

x_train = Float64.(x_data[p_order+1:end])[1:train_size];# Test set

x_prev_test = [Float64.(x_data[i+p_order-1:-1:i]) for i in 1:length(x_data)-p_order][train_size+1:end]

x_test = Float64.(x_data[p_order+1:end])[train_size+1:end];Inference

# Constraints are needed for performing VMP

arma_constraints = @constraints begin

q(z, h_0, h, η, τ, γ,e) = q(h_0)q(z, h)q(η)q(τ)q(γ)q(e)

end;# This cell defines prior knowledge for model parameters

h_prior = MvNormalMeanPrecision(zeros(q_order), diageye(q_order))

γ_prior = GammaShapeRate(1e4, 1.0)

τ_prior = GammaShapeRate(1e2, 1.0)

η_prior = MvNormalMeanPrecision(zeros(q_order), diageye(q_order))

θ_prior = MvNormalMeanPrecision(zeros(p_order), diageye(p_order));# Model's graph has structural loops, hence, it requires pre-initialisation

arma_initialization = @initialization begin

q(h_0) = h_prior

μ(h_0) = h_prior

q(h) = h_prior

μ(h) = h_prior

q(γ) = γ_prior

q(τ) = τ_prior

q(η) = η_prior

q(θ) = θ_prior

end

arma_meta = ar_meta(Multivariate, q_order, ARsafe());c = zeros(p_order); c[1] = 1.0; # AR

b = zeros(q_order); b[1] = 1.0; # MA

S = shift(q_order); # MA

result = infer(

model = ARMA(x_prev=x_prev_train, h_prior=h_prior, γ_prior=γ_prior, τ_prior=τ_prior, η_prior=η_prior, θ_prior=θ_prior, c=c, b=b, S=S),

data = (x = x_train, ),

initialization = arma_initialization,

constraints = arma_constraints,

meta = arma_meta,

iterations = 10,

options = (limit_stack_depth = 400, ),

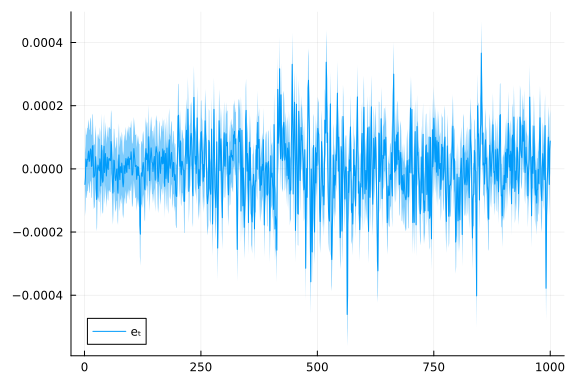

);plot(mean.(result.posteriors[:e][end]), ribbon = var.(result.posteriors[:e][end]), label = "eₜ")

# extract posteriors

h_posterior = result.posteriors[:h][end][end]

γ_posterior = result.posteriors[:γ][end]

τ_posterior = result.posteriors[:τ][end]

η_posterior = result.posteriors[:η][end]

θ_posterior = result.posteriors[:θ][end];Prediction

Here we are going to use our inference results in order to predict the dataset itself

# The prediction function is aimed at approximating the predictive posterior distribution

# It triggers the rules in the generative order (in future, RxInfer.jl will provide this function out of the box)

function prediction(x_prev, h_posterior, γ_posterior, τ_posterior, η_posterior, θ_posterior, p, q)

h_out = MvNormalMeanPrecision(mean(h_posterior), precision(h_posterior))

ar_out = @call_rule AR(:y, Marginalisation) (m_x=h_out, q_θ=η_posterior, q_γ=τ_posterior, meta=ARMeta(Multivariate, p, ARsafe()))

c = zeros(p); c[1] = 1.0

b = zeros(q); b[1] = 1.0

ar_dot_out = @call_rule typeof(dot)(:out, Marginalisation) (m_in1=PointMass(b), m_in2=ar_out)

θ_out = MvNormalMeanPrecision(mean(θ_posterior), precision(θ_posterior))

ma_dot_out = @call_rule typeof(dot)(:out, Marginalisation) (m_in1=PointMass(x_prev), m_in2=θ_out)

e_out = @call_rule NormalMeanPrecision(:out, Marginalisation) (q_μ=PointMass(0.0), q_τ=mean(γ_posterior))

ar_ma = @call_rule typeof(+)(:out, Marginalisation) (m_in1=ar_dot_out, m_in2=ma_dot_out)

@call_rule typeof(+)(:out, Marginalisation) (m_in1=ar_ma, m_in2=e_out)

endprediction (generic function with 1 method)predictions = []

for x_prev in x_prev_test

push!(predictions, prediction(x_prev, h_posterior, γ_posterior, τ_posterior, η_posterior, θ_posterior, p_order, q_order))

# after every new prediction we can actually "retrain" the model to use the power of Bayesian approach

# we will skip this part at this notebook

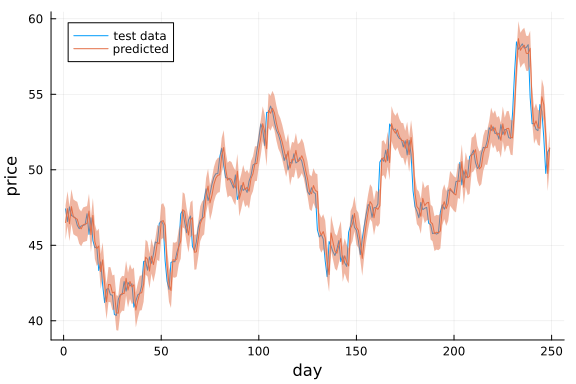

endplot(x_test, label="test data", legend=:topleft)

plot!(mean.(predictions)[1:end], ribbon=std.(predictions)[1:end], label="predicted", xlabel="day", ylabel="price")